An honest look at the pros, cons, and what to watch out for

When it comes to insulating your home, the options can be overwhelming. Spray foam has gained popularity over the years, but more recently it’s been under the spotlight for all the wrong reasons. From mortgage rejections to hidden structural damage, there’s a lot more to consider than just keeping heat in.

At Spray Foam Advice Centre, we specialise in helping homeowners navigate the complications that can come with spray foam—especially when things haven’t gone to plan. So if you're weighing up spray foam vs traditional insulation, here's what you really need to know.

1. Insulation Performance

Spray Foam:

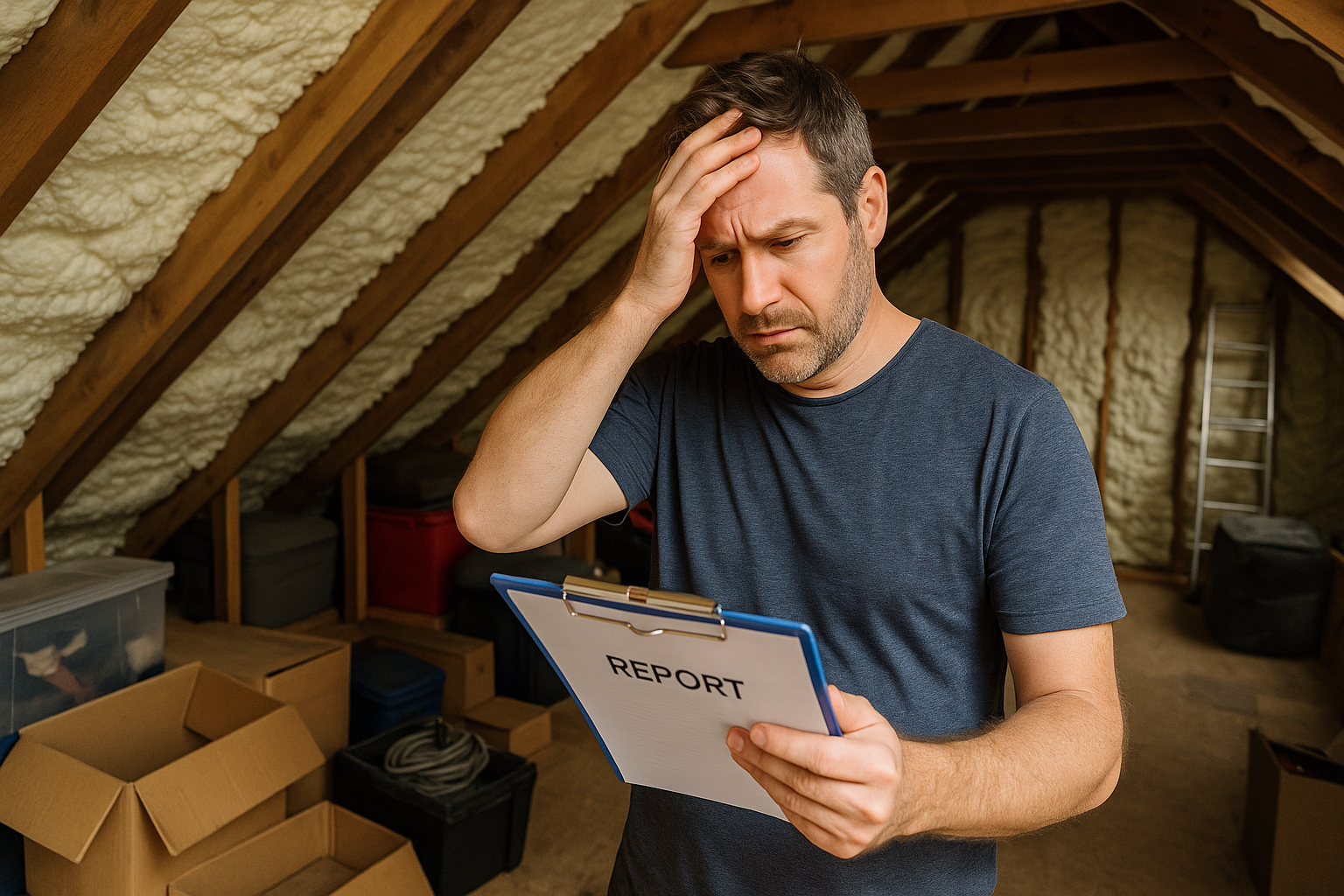

It performs well when correctly installed. Spray foam expands to fill gaps and can create an airtight seal, improving energy efficiency—but poor installation can cause condensation, trapped moisture, and damage to roof timbers.

Traditional Insulation:

Less airtight but more forgiving. It allows for some breathability in older homes and is easier to remove or top up if needed.

"An energy-efficient loft isn’t worth much if it comes with survey issues later."

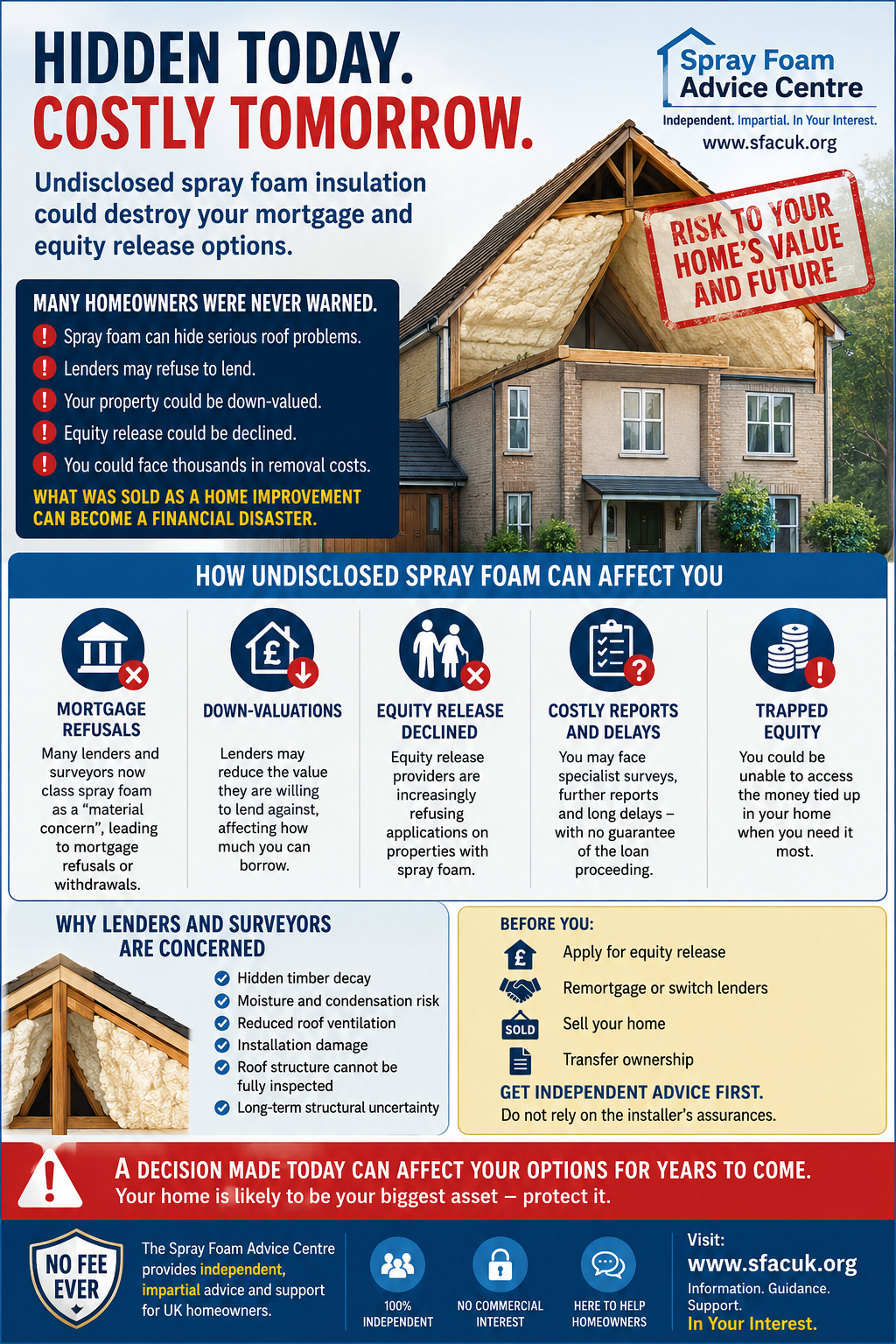

2. Property Value & Mortgage Issues

Spray Foam:

Many UK lenders still reject or require removal of spray foam insulation before offering a mortgage. Even open-cell foam can cause issues during surveys. In some cases, sales fall through completely due to its presence.

Traditional Insulation:

Lender-friendly and survey-safe. Rarely flagged as a problem.

"If you plan to sell or remortgage, spray foam can cause more harm than good without proper oversight—and even then, risk remains."

3. Cost & Longevity

Spray Foam:

Often sold as a ‘fit and forget’ solution—but removal can be costly and difficult if problems arise. If the installation is faulty, it doesn’t matter how efficient it could be.

Traditional Insulation:

Cheaper, simpler, and easier to maintain or replace if needed.

"Spray foam is only cost-effective when everything goes perfectly—and in our experience, it often doesn’t."

4. Breathability & Moisture Risk

Spray Foam:

Closed-cell foam in particular can block ventilation and trap moisture against roof timbers. Over time, this can lead to decay and costly structural repairs—especially in older homes not designed for airtight systems.

Traditional Insulation:

Breathable and easy to pair with natural airflow. Less likely to create hidden damp or condensation issues.

"Just because it’s warm doesn’t mean it’s healthy. Hidden damage is one of the biggest problems we see during removals."

5. Flexibility & Removal

Spray Foam:

Hard to reverse. Once installed, it’s bonded to timbers and can’t be peeled off like a roll of wool. If something goes wrong, removal is invasive and specialist.

Traditional Insulation:

Easy to upgrade, top up, or remove. No specialist tools or risk of structural damage.

So, Which One Should You Choose?

Spray foam insulation can work well—but only in the right property, under the right conditions, and with proper installation. Even then, future surveyors or mortgage lenders might disagree.

If you're considering it, get impartial advice first.

And if you already have spray foam and you’re facing issues, we can help you get clarity—and, if needed, safe removal.

Share this article