May 19, 2026

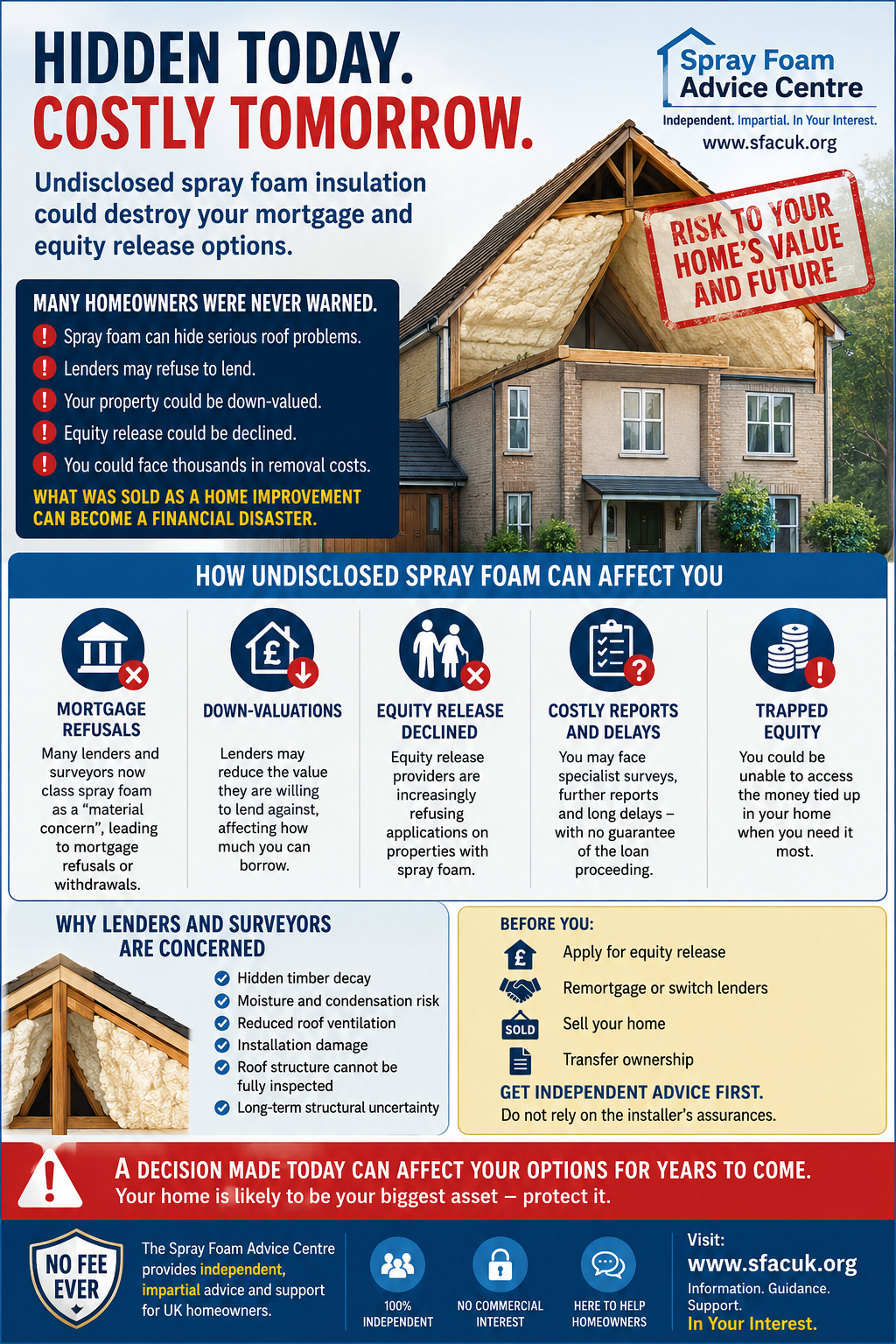

As the spray foam insulation crisis continues to affect homeowners across the UK, many people are only now discovering that they may have important legal protection under Section 75 of the Consumer Credit Act 1974. For some homeowners, this protection could prove financially life-changing. Why? Because if even part of the original spray foam installation was paid for using a credit card, homeowners may have the right to pursue claims not only for the installation itself — but potentially for associated losses, including costly removal work. At a time when many families are facing failed mortgage applications, equity release refusals, and expensive remediation bills, understanding Section 75 has become critically important. What Is Section 75? Section 75 of the Consumer Credit Act is a UK consumer protection law that makes credit card providers jointly liable for breaches of contract or misrepresentation by a retailer or service provider. In simple terms: If a company sold a product or service under misleading circumstances, and part of the payment was made using a credit card, the credit card company can also be held responsible. This protection applies even if: The company has ceased trading The installer refuses to help The warranty is worthless The homeowner only paid a deposit on the credit card Many consumers wrongly believe the entire balance must have been paid by credit card. That is not true. In many cases, paying just the initial deposit or first payment via credit card may be enough to trigger Section 75 protection. Why This Matters for Spray Foam Insulation Thousands of homeowners claim they were sold spray foam insulation without proper warnings about: Mortgage restrictions Lending refusals Future saleability concerns Ventilation risks Timber inspection limitations Potential removal costs Many homeowners state they were assured: “Mortgage lenders have no issue.” “The product is fully approved everywhere.” “It adds value to your home.” “It is completely safe for future buyers.” Years later, some are discovering: Their property is down-valued Equity release applications are declined Buyers cannot obtain mortgages Surveyors are flagging the roof structure Removal costs can exceed tens of thousands of pounds This is where Section 75 may become highly significant. Removal Costs May Also Form Part of a Claim One of the most important points homeowners should understand is this: Potential claims may not be limited solely to the original installation cost. If the product was misrepresented or sold without proper disclosure of foreseeable consequences, consequential losses may also be considered. This can include: Spray foam removal costs Roof timber inspection costs Surveyor reports Associated remedial works Financial losses linked to failed transactions Every claim is fact-specific, and outcomes vary, but legal and financial experts increasingly recognise that removal costs may form a substantial part of consumer claims where remediation becomes necessary to restore mortgageability. For homeowners now facing enormous removal bills simply to sell or refinance their homes, this aspect of Section 75 could be critical. The Key Requirement Many People Do Not Realise To qualify for Section 75 protection, one of the most important conditions is that at least part of the transaction must have been made directly using qualifying credit. In many spray foam cases, homeowners paid: The initial deposit by credit card Follow-up balances via bank transfer Finance agreements Debit cards Or cash The crucial point is this: If the first payment or deposit was made on a qualifying credit card, protection may still apply for the full contract value — not merely the deposit amount. This is one of the most misunderstood areas of consumer law. Homeowners Should Gather Evidence Immediately If you believe your property may be affected, it is important to begin collecting documentation as early as possible. Useful evidence may include: Original invoices Credit card statements Finance agreements Installation contracts Sales brochures Emails and WhatsApp messages Mortgage refusal letters Surveyor reports Removal quotations Guarantees and warranties Advertising claims made at the time of sale The stronger the documentary trail, the stronger the potential claim position may become. Time Is Important Many homeowners delay taking action because they assume: “Nothing can be done.” “The installer has disappeared.” “The warranty is useless.” “The problem is too old.” However, Section 75 protections can sometimes extend far beyond standard warranty periods. Each situation depends on individual facts, dates, and legal considerations, but homeowners should not automatically assume they have no options available. Awareness Could Save Homeowners Thousands For many families, spray foam insulation has become far more than an insulation issue. It has become: A lending issue A property value issue A retirement issue And in some cases, a financial survival issue Understanding Section 75 may offer an important pathway for homeowners facing unexpected financial harm linked to spray foam installations. The key message is simple: If you paid even part of the installation using a credit card, you may have more rights than you realise. Important Consumer Note This article is for general awareness only and does not constitute legal advice. Individual circumstances vary, and homeowners should seek independent legal and financial guidance regarding any potential claim. About The Spray Foam Advice Centre Spray Foam Advice Centre provides independent consumer awareness and guidance regarding spray foam insulation, mortgage concerns, remediation pathways, and homeowner support across the UK.