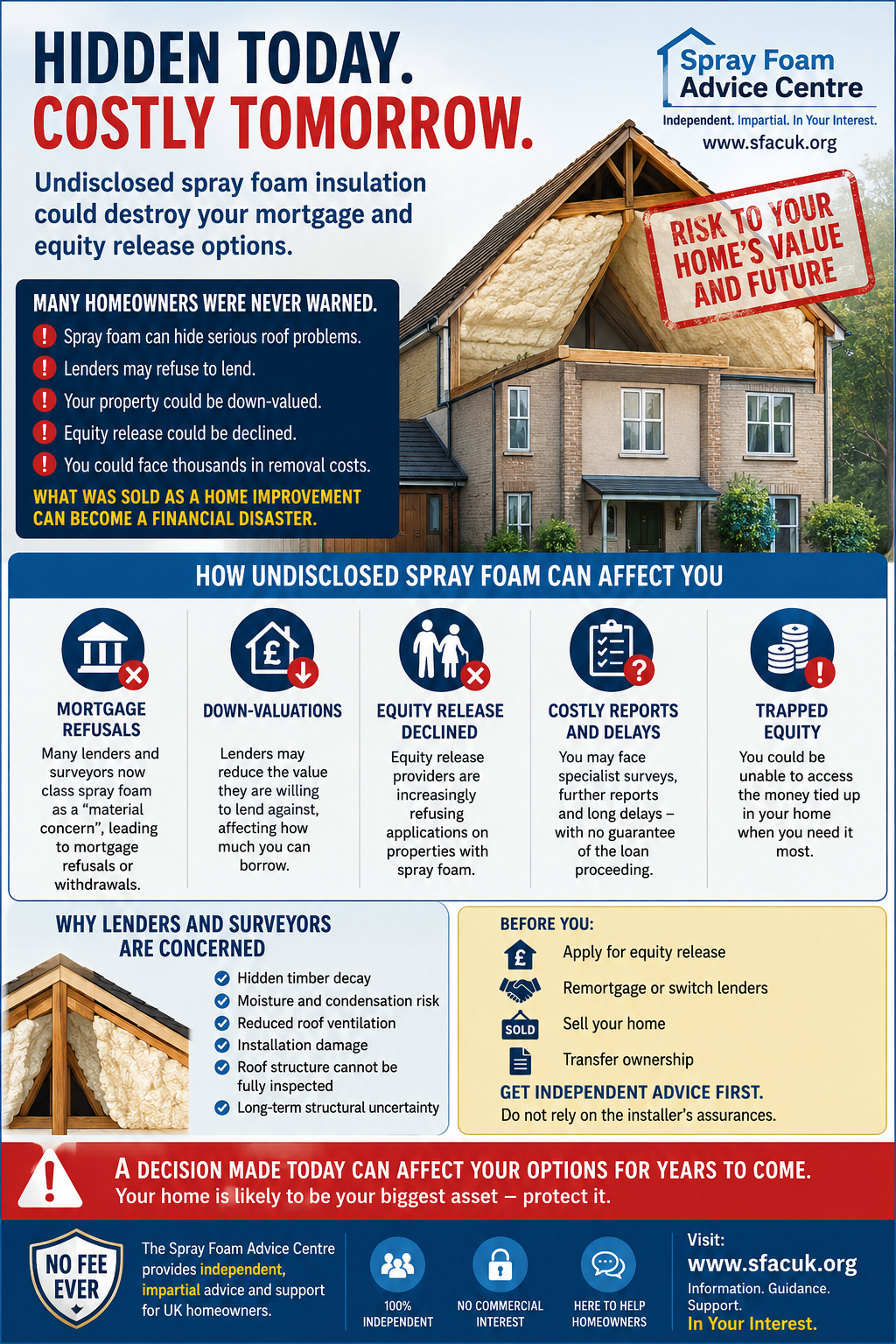

Mortgage Lenders Are Increasingly Refusing Spray Foam Properties

For many homeowners across the UK, spray foam insulation was sold as a modern solution — warmer homes, lower energy bills, and environmentally friendly efficiency. Salespeople promised savings, comfort, and increased energy performance. In some cases, elderly homeowners were actively targeted with promises of “government-backed schemes” or “urgent insulation upgrades.”

But today, thousands of homeowners are discovering a devastating reality.

What they believed was a home improvement may now be turning their property into an unmortgageable asset.

And for many pensioners and vulnerable homeowners relying on equity release, remortgaging, or downsizing in later life, the consequences are becoming financially catastrophic.

Mortgage Lenders Are Increasingly Refusing Spray Foam Properties

Across the UK, mortgage lenders and equity release providers have become increasingly cautious about properties containing spray foam insulation — particularly spray foam applied directly to the underside of roof tiles or within loft structures.

Why?

Because lenders and surveyors are concerned about several key risks:

- Hidden timber decay

- Moisture retention and condensation

- Inability to properly inspect roof structures

- Damage caused during installation or removal

- Reduced roof ventilation

- Long-term structural uncertainty

In many cases, surveyors instructed by lenders are now flagging spray foam installations as a “material concern,” leading to:

- Mortgage refusals

- Down-valuations

- Retentions

- Demands for specialist reports

- Or complete withdrawal of lending offers

For homeowners who were never warned about these risks at the point of sale, the shock can be enormous.

The Equity Release Time Bomb

The issue becomes even more serious when homeowners reach retirement age.

Many older homeowners rely on equity release products or later-life lending to:

- Clear debts

- Fund care costs

- Supplement pensions

- Help family members

- Remain financially secure in retirement

But if a lender refuses to lend against a property containing spray foam insulation, that equity can effectively become trapped.

Imagine owning a house worth £300,000 on paper — but being unable to release any of its value because lenders view the roof as a liability.

For some homeowners, this creates an impossible situation:

- They cannot access funds.

- They cannot easily sell.

- Buyers cannot secure mortgages.

- Equity release providers decline applications.

- And removal costs can run into many thousands of pounds.

The result is financial paralysis.

Some Homeowners Were Never Properly Informed

One of the most concerning aspects of this growing crisis is the number of homeowners who claim they were never adequately warned about future mortgage implications.

Many installations were sold using aggressive or misleading sales tactics, including claims such as:

- “Mortgage lenders have no issue with spray foam.”

- “It increases property value.”

- “It is fully approved everywhere.”

- “It is the same as traditional insulation.”

- “This will help you sell your property.”

In reality, lending policies can vary dramatically between providers, and many homeowners were never advised to seek independent mortgage or legal advice before installation.

In some cases, installers disappeared years later, leaving homeowners facing major financial consequences with little support.

Why Surveyors Are Concerned

Surveyors are not simply rejecting spray foam properties without reason.

Closed-cell and open-cell spray foams can make roof inspections significantly more difficult. Timber rafters, felt membranes, and hidden defects may no longer be visible once foam has bonded to the structure.

This creates uncertainty for lenders.

A mortgage provider lending hundreds of thousands of pounds against a property wants confidence that:

- The roof structure is sound

- No hidden decay exists

- Repairs will not become excessively expensive

- The property remains saleable in the future

If those assurances cannot be provided, the lender may simply walk away from the deal.

The Human Cost Is Growing

Behind every refused mortgage is a real homeowner.

Many are elderly.

Many acted in good faith.

Many believed they were improving their homes.

Now, homeowners across the UK are reporting:

- Failed house sales

- Collapsed chains

- Mortgage rejections

- Equity release refusals

- Severe financial stress

- Anxiety and mental health strain

- Unexpected removal quotes running into tens of thousands of pounds

Some families are discovering the issue only after bereavement, when trying to sell inherited properties.

Others are trapped in homes they can no longer refinance or move from.

Homeowners Must Start Asking Questions

If your property has spray foam insulation installed, particularly within the loft or roof structure, it is essential to understand the potential implications before:

- Applying for equity release

- Selling your home

- Remortgaging

- Switching lenders

- Transferring ownership

Key questions include:

- Was the installation properly documented?

- Was ventilation correctly maintained?

- Is there independent certification?

- Can the roof structure still be fully inspected?

- Will your intended lender accept the installation?

Do not rely solely on the original installer’s assurances.

Seek independent professional advice from qualified surveyors, mortgage professionals, and specialist remediation experts where appropriate.

Awareness Is Critical

The purpose of raising awareness is not to create panic.

Not every spray foam installation automatically means a property is unmortgageable. Lending decisions vary between lenders, surveyors, foam types, and installation quality.

However, the issue is now significant enough that homeowners deserve transparency before making decisions that could affect the future value and financeability of their property.

For many people, their home is their largest asset.

Understanding how spray foam insulation may impact mortgages and equity release is no longer optional — it is essential.

About The Spray Foam Advice Centre

Spray Foam Advice Centre provides independent consumer awareness and guidance regarding spray foam insulation, mortgage concerns, remediation pathways, and homeowner support across the UK.

Need Help?

Share this article