Why Spray Foam Causes Problems at Sale

Selling a home in the UK already involves enough paperwork, negotiations, and delays. But if your property has spray foam insulation installed in the roof, you could be facing an additional hurdle that many homeowners are not prepared for.

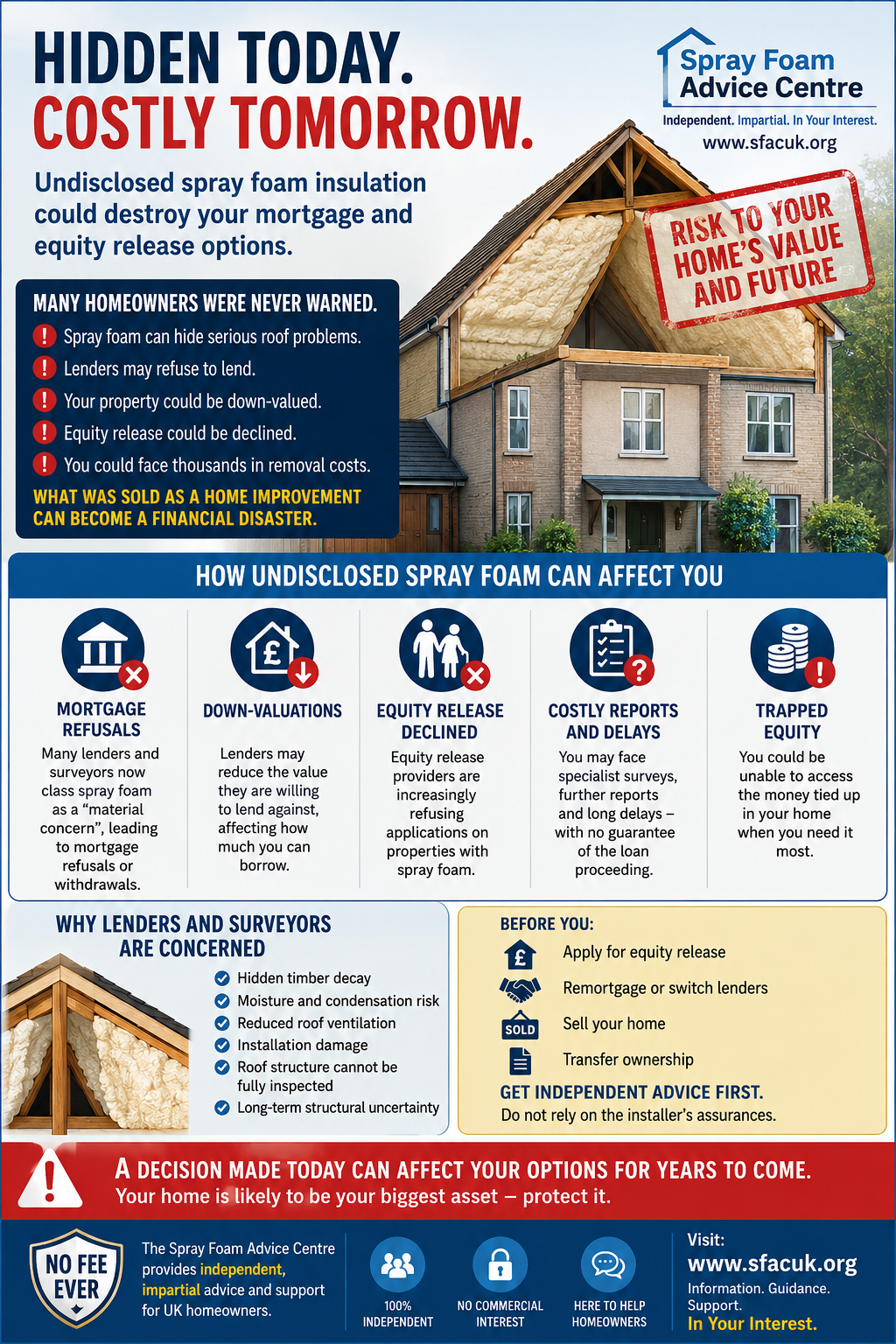

Spray foam insulation has been promoted for years as an energy-saving product. Unfortunately, it is now one of the most common reasons a sale falls through during the conveyancing and mortgage process. Almost every high-street mortgage lender in the UK has strict conditions, and many will decline a mortgage outright if spray foam is present.

Why Spray Foam Causes Problems at Sale

- Surveyor’s Duty of Care

When a purchaser applies for a mortgage, the lender instructs a surveyor to carry out a property valuation or a HomeBuyer Report. The surveyor must assess whether the property is suitable for lending security. - If spray foam is identified, the surveyor cannot see the condition of the underlying timbers or ventilation pathways. This lack of visibility means the surveyor has to report it as a risk of hidden damage (condensation, timber decay, roof structure failure).

- Mortgage Lender Policies

Most lenders will not accept spray foam insulation because of the potential for hidden defects. Even if your roof is in excellent condition, the surveyor will still have to note it as a defect, and the mortgage application is likely to be declined. - The Cost of Finding Out Too Late

A pre-sale survey or mortgage valuation typically costs £400–£600. If spray foam is present, the report will almost certainly flag it as a significant issue, yet you will still have paid the full fee for the inspection. The buyer may then walk away, leaving you back at square one.

How to Avoid Wasting Time and Money

Instead of waiting until the buyer’s surveyor finds the issue, you can be proactive. The Spray Foam Advice Centre offers specialist guidance before you list your property for sale.

- ✅ Pre-sale consultation – We can advise you on whether the spray foam is likely to be a barrier to sale.

- ✅ Removal guidance – If removal is required, we can connect you with trusted removal contractors who understand lender requirements.

- ✅ Surveyor-ready documentation – We help you prepare your property so that when a surveyor attends, they can issue a clean report without flagging spray foam as a defect.

By taking advice early, you could save hundreds of pounds in wasted survey fees and avoid the stress of losing potential buyers.

The Bottom Line

If you are planning to sell your home and it contains spray foam insulation, do not wait until the buyer’s survey flags it as a problem. Once spray foam is reported, the sale is likely to collapse unless the insulation is removed and the roof reinstated to a lender-approved standard.

Speaking to the Spray Foam Advice Centre before you go to market can make the difference between a smooth sale and months of delay.

Contact us today for clear advice and a route forward – before you spend money on surveys that will only highlight the problem.

Share this article