Key Reasons for Mortgage Difficulties

Why Can't I Get a Mortgage with Spray Foam Insulation?

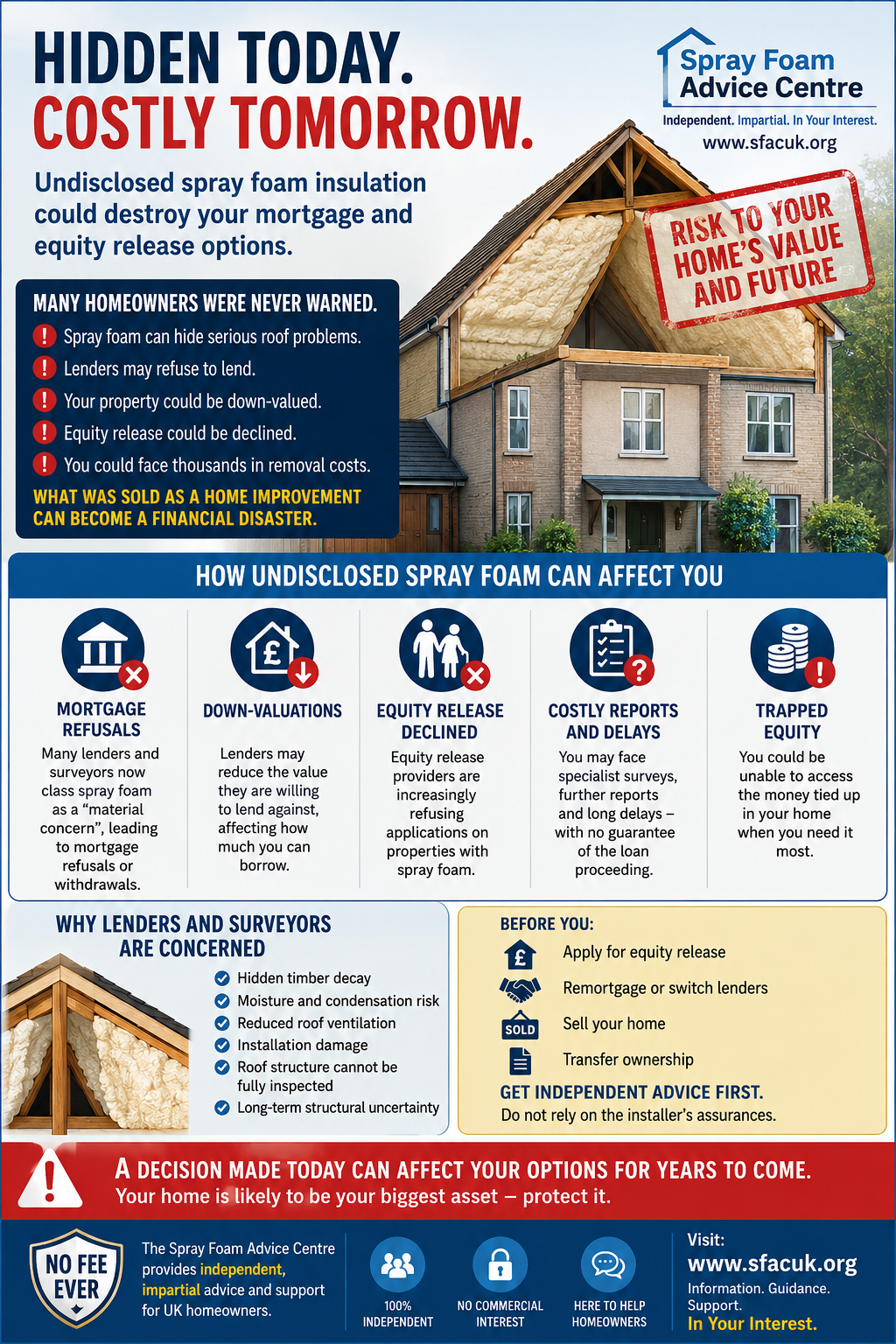

Spray foam insulation has gained popularity in the construction and home renovation industries due to its outstanding insulating properties, energy efficiency, and ability to create a seamless barrier against air and moisture. However, homeowners considering this method may encounter an unexpected obstacle when applying for a mortgage: difficulty securing financing. This article explores the reasons why homes insulated with spray foam may face challenges in the mortgage approval process and offers guidance on how to navigate these issues.

Understanding Spray Foam Insulation

Spray foam insulation comes in two primary types: open-cell and closed-cell foam. Open-cell foam is lightweight and has a lower R-value but provides excellent soundproofing and air-sealing capabilities. Closed-cell foam is more dense, has a higher R-value, and serves as a vapor barrier, making it ideal for damp environments.

While spray foam insulation is widely celebrated for its energy efficiency and effectiveness, the use of this material has raised concerns among lenders and industry professionals.

Key Reasons for Mortgage Difficulties

1. Lack of Compliance with Building Codes

One of the main reasons lenders may be hesitant to approve mortgages for homes with spray foam insulation is non-compliance with local building codes. In some cases, spray foam may not be installed according to manufacturer guidelines or local regulations, which can lead to serious issues, including:

- **Structural Compromise:** Improper installation can create weaknesses in the building structure, which may lead to costly repairs.

- **Health Risks:** Poorly installed spray foam can result in off-gassing, producing harmful chemicals and diminishing indoor air quality. This can present health risks to the occupants.

- **Moisture Issues:** If the insulation traps moisture in walls or ceilings, it can lead to mold growth and long-term damage to the home.

Lenders want to ensure that the homes they finance are safe, secure, and compliant with local codes. Therefore, if a property does not meet these requirements due to defective spray foam insulation, it may be deemed unmortgageable.

2. Concerns About Resale Value

Another factor impacting mortgage eligibility is the perception that homes with spray foam insulation may have compromised resale value. Real estate appraisers and home inspectors may view properties with improperly installed spray foam as a potential liability. If they determine that the insulation could lead to future problems, they may appraise the home at a lower value, impacting the lender’s willingness to extend financing.

Moreover, if a real estate buyer is concerned about the risks associated with spray foam insulation, they may decide against purchasing the property altogether. This may create a cyclical issue: as fewer buyers are willing to purchase homes with spray foam insulation, the overall demand and market value decrease.

3. Limited Lender Familiarity

Not all lenders are well-versed in spray foam insulation, leading to uncertainty about financing properties that utilize it. Lenders typically have standard practices and guidelines for evaluating properties, but spray foam insulation can fall outside these norms.

If a lender is unfamiliar with spray foam and its benefits, they may err on the side of caution and choose not to finance the property. In some cases, lenders may require additional inspections or documentation, which can delay the approval process or lead to outright denials.

4. Difficulties with Insurance

Insurance underwriting often plays a crucial role in the mortgage approval process, and insurance companies may be wary of homes insulated with spray foam. If the home is deemed high-risk due to improper installation or potential moisture issues, homeowners may find it challenging to obtain homeowner’s insurance.

Without proper insurance coverage, lenders may be reluctant to approve a mortgage application. Additionally, if the spray foam insulation leads to higher insurance premiums, it may further deter potential buyers.

5. Regulatory and Environmental Concerns

Some types of spray foam insulation contain chemicals that can be harmful to human health and the environment. As environmental regulations become stricter, lenders may be cautious about financing homes that utilize potentially hazardous materials.

If a property is seen as an environmental risk, mortgage approvals could be affected. This concern is especially relevant in markets where eco-friendliness and sustainability are highly valued.

Steps to Take if You Have Spray Foam Insulation

If you currently own a home with spray foam insulation or are considering purchasing one, you can take several steps to mitigate potential mortgage issues:

1. Ensure Proper Installation

Before applying for a mortgage, verify that your spray foam insulation was installed by a qualified professional following all manufacturer guidelines and relevant building codes. Retain documentation of the installation process, including receipts, contracts, and any inspections.

2. Conduct an Inspection

Consider hiring a reputable home inspector or energy auditor with experience in evaluating spray foam insulation. An inspection can help identify any potential issues with the insulation, allowing you to rectify problems before seeking mortgage approval.

3. Provide Documentation

When applying for a mortgage, gather all relevant documentation related to the spray foam insulation, including installation certificates and inspection reports. Presenting comprehensive records can help assure lenders that the insulation is compliant with building codes

By,

Adam Gough - Spray Foam Advice Centre

Share this article